In today's digital economy, handling cardholder data is both a necessity and a significant responsibility. Failure to protect this sensitive information can lead to catastrophic data breaches, severe financial penalties, and irreparable damage to your brand reputation. This is where the Payment Card Industry Data Security Standard (PCI DSS) comes into play. It’s not just a set of rules; it's a critical framework for building a secure payment environment that protects your customers and your business.

Navigating its 12 core requirements, however, can be a complex and resource-intensive task, especially for growing fintech platforms, e-commerce stores, and enterprise systems undergoing modernization. Many organizations struggle with understanding where to start, what evidence to collect, and how to translate abstract requirements into concrete technical controls. For a concise overview of how to navigate these requirements, you might find this quick PCI DSS compliance checklist guide helpful.

This comprehensive PCI DSS compliance checklist is designed to cut through the complexity. We will break down each of the 12 requirements into actionable steps, highlight common pitfalls, and provide practical insights for implementation. Our goal is to move beyond generic advice and offer a strategic roadmap that helps you not only achieve compliance but also build a resilient, scalable, and secure infrastructure. This guide will transform a daunting regulatory hurdle into a clear, manageable process that fosters lasting customer trust.

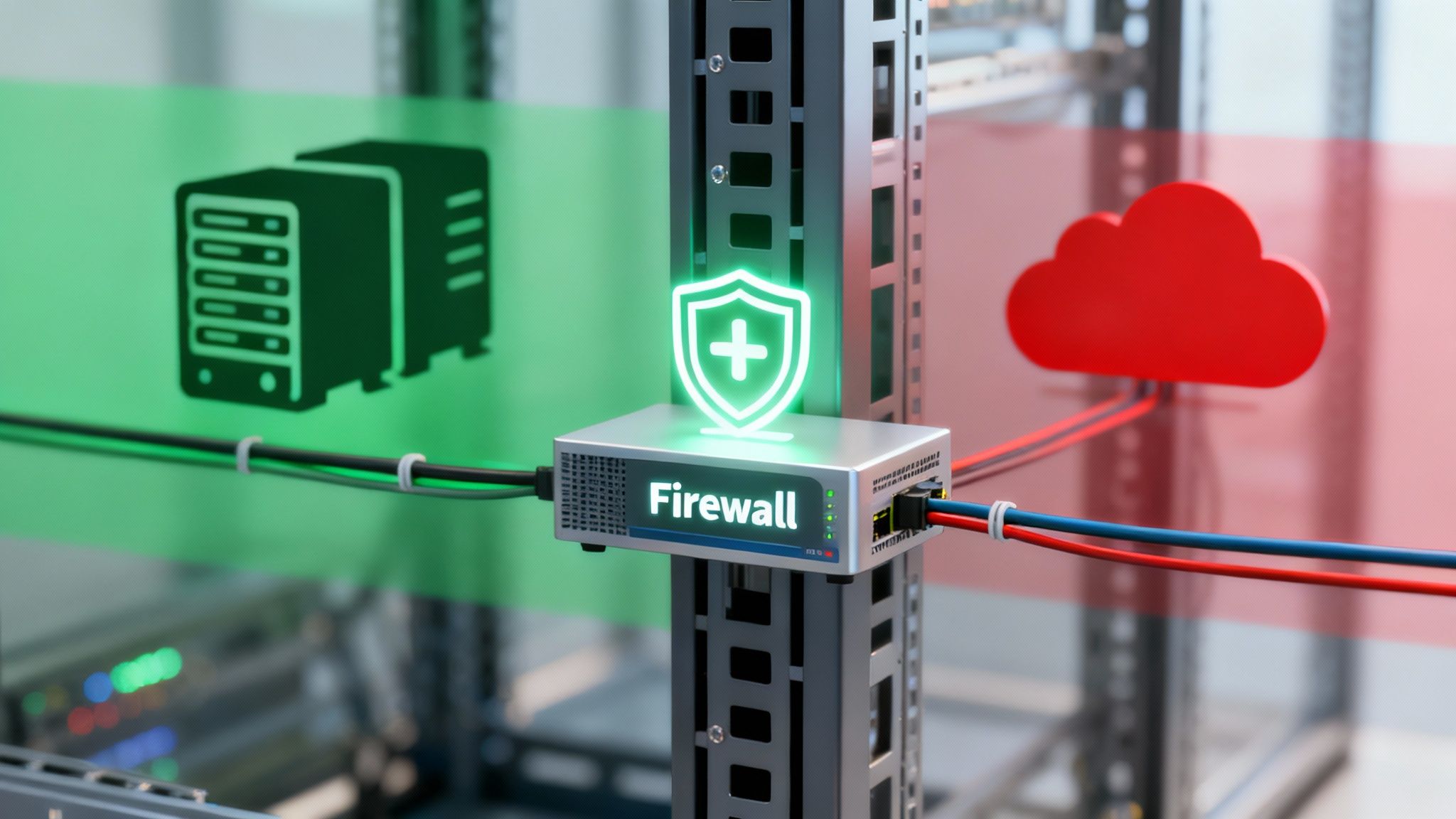

1. Requirement 1: Install and Maintain a Firewall Configuration

Firewalls are your first line of defense in a PCI DSS compliance checklist, acting as a critical barrier between your secure internal network and untrusted external networks like the internet. This requirement mandates establishing and maintaining secure firewall and router configurations to protect the Cardholder Data Environment (CDE). The primary goal is to control all network traffic, permitting only legitimate business traffic while explicitly denying everything else.

Properly configuring and maintaining a firewall is the first critical step, and understanding your options for choosing the best firewalls for small business can significantly strengthen your security posture. A robust configuration ensures that any system component storing, processing, or transmitting cardholder data is shielded from unauthorized access.

Actionable Steps and Evidence

- Document and Justify All Rules: Maintain a formal document listing every firewall rule with a clear business justification for each one. Auditors will ask for this.

- Implement a Default-Deny Policy: Configure your firewalls to block all traffic by default and then create specific rules to allow only necessary services, protocols, and ports. This "deny-all" approach minimizes your attack surface.

- Segment Your Network: Isolate the CDE from the rest of your corporate network using firewalls. A fintech platform, for instance, might place its transaction processing servers in a highly restricted DMZ, protected by multiple firewall layers.

- Regular Rule Reviews: Conduct and document quarterly reviews of all firewall and router rule sets. The purpose is to identify and remove obsolete or unnecessary rules that could create security gaps.

2. Requirement 2: Do Not Use Vendor-Supplied Defaults for System Passwords and Other Security Parameters

Network devices, servers, and software applications frequently ship with generic, publicly known default passwords and security settings. This requirement is a foundational element of any PCI DSS compliance checklist, as it mandates the immediate replacement of all vendor-supplied defaults before any system is installed in the Cardholder Data Environment (CDE). Attackers actively use lists of these default credentials to gain initial, unauthorized access to networks.

Changing default passwords like "admin/admin" or "root/password" is the bare minimum. This requirement extends to hardening all security parameters, such as disabling unnecessary services, closing unused ports, and removing default accounts. For example, a fintech platform deploying a new payment gateway would ensure all default administrative accounts are removed and new, unique credentials are created as part of their standardized server build process. This proactive hardening significantly reduces the low-hanging fruit that attackers exploit.

Actionable Steps and Evidence

- Establish Hardened Configurations: Create and maintain secure, documented configuration standards for all system components. These standards must address all known security vulnerabilities and be consistent with industry-accepted hardening practices.

- Change All Defaults Before Deployment: Before installing a system on the network, always change all wireless vendor defaults, including default encryption keys, passwords, and SNMP community strings.

- Disable or Remove Unnecessary Defaults: Disable or remove all unnecessary default accounts, services, and functionality before any system component goes live. Document these changes in your configuration standards.

- Maintain an Inventory: Keep a detailed inventory of all system components within the CDE and ensure that their configurations are documented and that all default credentials have been changed. This inventory is critical for audit purposes.

3. Requirement 3: Protect Stored Cardholder Data

Protecting cardholder data at rest is a non-negotiable part of the PCI DSS compliance checklist. This requirement mandates that any stored Primary Account Number (PAN) must be rendered unreadable wherever it is stored. The core objective is to ensure that even if a bad actor breaches your storage systems, the compromised data is encrypted and completely useless to them.

Implementing strong cryptographic controls is fundamental. This involves using industry-tested algorithms, secure key management protocols, and other protective measures like truncation or tokenization. Selecting the right encryption method is crucial; understanding the differences between cryptographic standards is an essential first step. You can explore a detailed comparison between AES vs. RSA encryption to make an informed decision for your environment.

Actionable Steps and Evidence

- Implement Strong Cryptography: Encrypt all stored PAN data using industry-accepted algorithms like AES-256. For example, a fintech platform might use AWS RDS with encryption at rest enabled to protect customer databases.

- Secure Encryption Keys: Store cryptographic keys separately from the encrypted data in a secure, isolated environment. Using a Hardware Security Module (HSM) is the best practice for protecting and managing keys.

- Minimize Data Storage: Implement data retention policies to ensure you only store cardholder data for the minimum time required for legal, regulatory, or business needs. Never store sensitive authentication data (SAD) after authorization.

- Use Masking, Truncation, or Tokenization: Display the PAN only when absolutely necessary and mask it otherwise (e.g., showing only the last four digits). Use truncation or tokenization to further minimize the risk associated with data storage.

4. Requirement 4: Encrypt Cardholder Data in Transit Across Public Networks

Cardholder data becomes incredibly vulnerable the moment it travels outside your secure internal network. Requirement 4 of the PCI DSS compliance checklist addresses this by mandating strong cryptography for all transmissions of cardholder data across open, public networks like the internet. This ensures that even if malicious actors intercept the data, they cannot read or use it, protecting information sent from payment terminals, customer browsers, and between your servers and third-party processors.

The core principle is to make sensitive data unreadable during its journey. This is achieved by using secure, validated encryption protocols and strong cipher suites. For instance, a payment gateway enforcing TLS 1.2 or higher for all API communications and an e-commerce platform using HSTS headers to force encrypted connections are both prime examples of meeting this critical requirement. Proper implementation prevents man-in-the-middle attacks and eavesdropping, preserving the confidentiality and integrity of cardholder data.

Actionable Steps and Evidence

- Enforce Strong Transport Layer Security (TLS): Disable all outdated and insecure protocols such as SSL v3.0, TLS 1.0, and TLS 1.1. Your documented security policies must mandate a minimum of TLS 1.2, with TLS 1.3 strongly recommended for new implementations.

- Use Strong Cipher Suites and Valid Certificates: Maintain a list of approved, strong cryptographic cipher suites and ensure weak algorithms (like RC4, MD5, SHA-1) are explicitly disabled. Use SSL/TLS certificates only from trusted Certificate Authorities (CAs) and establish an automated process for monitoring and renewing them before they expire.

- Protect All Sensitive Transmissions: The encryption mandate extends beyond just payment transactions. Ensure all transmissions of cardholder data are encrypted, including those over email, instant messaging, or remote administrative access.

- Conduct Regular Configuration Audits: Periodically use tools like SSL Labs to scan your public-facing servers. Keep records of these scans as evidence that your configurations are secure, certificates are valid, and no weak protocols or ciphers are in use.

5. Requirement 5: Protect Systems Against Malware and Maintain Anti-Malware Software

Malware, including viruses, spyware, and trojans, poses a direct threat to cardholder data. Requirement 5 of this PCI DSS compliance checklist mandates the deployment and active maintenance of anti-malware solutions on all systems commonly affected by malicious software. This protection is critical for preventing unauthorized access, data theft, and system compromises that could lead to a catastrophic breach of cardholder data.

Effective anti-malware is not a "set it and forget it" control. It requires a comprehensive strategy that covers all endpoints within the Cardholder Data Environment (CDE), including servers, workstations, and even mobile devices. The goal is to detect, remove, and protect against all known types of malware, ensuring the integrity of your payment processing systems. For instance, a fintech platform might deploy a centrally managed Endpoint Detection and Response (EDR) solution to gain advanced threat protection and real-time visibility across its entire infrastructure.

Actionable Steps and Evidence

- Deploy Comprehensive Coverage: Install anti-malware software on all systems within the CDE and any system that could impact its security. This includes web servers, database servers, and employee workstations.

- Ensure Continuous Operation: Configure anti-malware solutions to be active at all times and ensure that users cannot disable or alter them. Centralized management tools like Microsoft Intune for Windows Defender are essential for enforcement.

- Maintain Automatic Updates: Ensure all anti-malware solutions automatically receive signature and engine updates at least daily. This is a common point of failure that auditors will verify by checking update logs.

- Conduct Regular Scans: Implement and document periodic scans of all protected systems. Supplement these with real-time scanning for high-risk activities like accessing web-based email or removable media.

- Document Malware Incidents: Maintain detailed logs of all malware detection events. Your evidence should include the alert, the investigation process, and the remediation actions taken to neutralize the threat and prevent recurrence.

6. Requirement 6: Develop and Maintain Secure Systems and Applications

Security vulnerabilities are often introduced during the development process, making this requirement a cornerstone of a proactive PCI DSS compliance checklist. It mandates that organizations establish and follow formal processes to build and maintain secure software and systems. This involves embedding security into every phase of the development lifecycle, from initial design to post-deployment maintenance, to protect the Cardholder Data Environment (CDE) from common exploits.

This requirement applies to both custom-developed applications and third-party software. For instance, a fintech platform must ensure its internally built payment APIs adhere to secure coding standards like the OWASP Top 10. Similarly, it must have a process to promptly apply security patches to all commercial software, such as operating systems or web servers, used within the CDE. The goal is to minimize the attack surface by systematically identifying and remediating vulnerabilities before they can be exploited.

Actionable Steps and Evidence

- Establish a Secure SDLC: Document and implement a formal Secure Software Development Lifecycle (SDLC) that integrates security checks at each stage, from requirements gathering to deployment.

- Provide Secure Coding Training: Train all developers annually on secure coding best practices, focusing on common vulnerabilities like SQL injection, Cross-Site Scripting (XSS), and insecure authentication. Document training completion for auditors.

- Implement Vulnerability Management: Use automated tools for both static (SAST) and dynamic (DAST) application security testing. A DevOps team might integrate a tool like SonarQube into their CI/CD pipeline to automatically scan code for flaws before it reaches production.

- Patch Promptly: Develop a formal process for identifying and classifying new security vulnerabilities. Ensure critical security patches are applied within one month of release, and maintain logs as evidence of timely patching.

7. Requirement 7: Implement Strong Access Control Measures and Restrict Access by Business Need to Know

This requirement is centered on the principle of least privilege, which dictates that personnel should only have the absolute minimum access to data and systems necessary to perform their job functions. To complete this section of your PCI DSS compliance checklist, you must restrict access to cardholder data based on a well-defined "need-to-know" basis. Every user, application, and system component must have its access rights strictly limited to its specific, documented business purpose.

The goal is to prevent unauthorized access and potential misuse of sensitive information by ensuring that every access grant is justified and documented. For example, a fintech platform would implement role-based access control (RBAC), giving customer service agents read-only access to transaction histories while restricting database administrators from viewing full primary account numbers. This granular control is fundamental to protecting the Cardholder Data Environment (CDE).

Actionable Steps and Evidence

- Implement a Default-Deny Policy for Access: All access to the CDE should be denied by default. Privileges must be explicitly and formally granted based on a user's specific job role and responsibilities.

- Establish a Formal Access Control System: Use a system like Role-Based Access Control (RBAC) to manage permissions. Document all roles and their associated privileges. For instance, Group 107 implements privileged access management for fintech client infrastructure to enforce these controls.

- Document and Justify All Access: Maintain records of all access requests, approvals, and the business justification for each one. Auditors will verify that every user with access has a legitimate need.

- Conduct Regular Access Reviews: Perform and document access reviews at least quarterly. The goal is to verify that all existing access is still required and appropriate for each user's current role, removing any unnecessary permissions.

- Immediate Revocation of Access: Have a formal process to immediately disable access for terminated employees or those who have changed roles. This prevents orphaned accounts from becoming a security risk.

8. Requirement 8: Identify and Authenticate Access to System Components

This requirement is foundational to a secure PCI DSS compliance checklist, as it ensures every user and process is uniquely identified and authenticated before accessing system components. The core principle is accountability; if you cannot prove who accessed what and when, you cannot enforce access controls or trace malicious activity. This involves assigning a unique ID to every individual and implementing strong authentication mechanisms to verify their identity.

The goal is to move beyond shared or generic accounts, which make it impossible to attribute actions to a specific person. By enforcing unique identification, organizations can create clear audit trails and ensure that access is granted on a strict need-to-know basis. For example, a fintech platform might use hardware security tokens for high-privilege administrative access, ensuring that only authorized personnel can make critical system changes.

Actionable Steps and Evidence

- Implement Unique IDs: Assign a unique identification (user ID) to each person with access to system components. Prohibit the use of shared or generic accounts and credentials.

- Enforce Strong Authentication: Implement multi-factor authentication (MFA) for all remote network access originating from outside the network and for all administrative access into the CDE. You can learn more about various biometric authentication methods to enhance security.

- Secure All Credentials: Use strong cryptography to render all authentication credentials (like passwords/passphrases) unreadable during transmission and storage on all system components.

- Manage User Accounts: Maintain a formal process for adding, modifying, and deleting user accounts. This includes immediately revoking access for terminated users and disabling inactive accounts within 90 days.

- Enforce Password Policies: Configure systems to enforce strong password parameters, including a minimum length of 12 characters, complexity requirements, and account lockout after no more than six failed login attempts.

9. Requirement 9: Restrict Physical Access to Cardholder Data

While digital threats are often top of mind, this part of the PCI DSS compliance checklist addresses the foundational need to secure the physical environment. Requirement 9 mandates that organizations control all physical access to facilities, systems, and equipment that store, process, or transmit cardholder data. This prevents unauthorized personnel from gaining hands-on access to sensitive infrastructure, which could lead to data theft, tampering, or device compromise.

The scope of this requirement covers everything from on-premise data centers and server rooms to office spaces where payments are handled and secure storage locations for media. For example, a financial institution must ensure not only its server racks are locked but also that any paper documents or backup tapes containing cardholder data are stored in secure, access-controlled areas. Effective physical security is a non-negotiable layer of defense that underpins all logical and network security controls.

Actionable Steps and Evidence

- Implement Multi-Layered Access Control: Use appropriate entry controls to restrict access to sensitive areas. This could involve badge readers for an office, progressing to multi-factor authentication (e.g., badge + biometric scan) for a data center.

- Maintain and Monitor Visitor Access: Create and enforce a formal visitor policy. This includes maintaining a log of all visitors, issuing them temporary identification badges that expire, and ensuring they are escorted at all times within secure zones.

- Install and Monitor Video Surveillance: Deploy cameras at all entry and exit points of sensitive areas like server rooms. Regularly review and retain footage as per your data retention policy to investigate any physical security incidents.

- Secure All Media: Develop strict procedures for the storage, distribution, and destruction of all media containing cardholder data. This includes securely storing backup tapes in an off-site location and using cross-cut shredders, incineration, or degaussing services to destroy media that is no longer needed.

10. Requirement 10: Track and Monitor Access to Network Resources and Cardholder Data

Without a detailed audit trail, identifying a breach or tracing unauthorized activity is nearly impossible. This requirement in the PCI DSS compliance checklist mandates the implementation of comprehensive logging and monitoring for all access to network resources and cardholder data. The core goal is to create a clear, chronological record of events, which is essential for detecting security incidents, conducting forensic investigations, and verifying that security controls are working as intended.

Effective logging acts as a digital surveillance system for your CDE. For example, a banking platform might log every single database query to its payment tables, including the user, timestamp, and query content. This level of detail ensures accountability and provides the necessary evidence to reconstruct events after a security incident. An effective strategy often involves leveraging a Security Information and Event Management (SIEM) solution to centralize and analyze these logs in real-time.

Actionable Steps and Evidence

- Implement Detailed Logging: Ensure all system components log access to cardholder data, including user identification, event type, date, time, and success or failure indication. All administrative actions must also be logged.

- Centralize Log Management: Use a SIEM tool like Splunk or Microsoft Sentinel to aggregate logs from all systems within the CDE. This simplifies analysis, correlation, and alerting across disparate sources.

- Protect Log Integrity: Implement measures to prevent log tampering. This can include using write-once media, ensuring logs are sent to a secure, segregated server, and enabling file-integrity monitoring on log files.

- Establish a Review Cadence: Formally conduct and document daily log reviews for critical systems and at least weekly for all others. Use automated alerting for suspicious patterns, such as multiple failed logins or access attempts outside business hours.

- Define Retention Policies: Retain audit trail history for at least one year, with a minimum of the last three months immediately available for analysis. Document and automate this log retention and archival process.

11. Requirement 11: Regularly Test Security Systems and Processes

Static security is no security at all. Requirement 11 mandates that you regularly test security systems and processes to ensure they are effective and functioning as intended. This is a proactive measure in any PCI DSS compliance checklist, designed to identify vulnerabilities before malicious actors can exploit them. It encompasses a range of activities, from vulnerability scanning and penetration testing to intrusion detection and file-integrity monitoring.

This requirement verifies that the security controls you have implemented are not just present but are actively working to protect the Cardholder Data Environment (CDE). For example, a fintech platform might use continuous vulnerability scanning in its CI/CD pipeline to catch security flaws before they ever reach production, supplementing this with annual, in-depth penetration tests from a third-party firm. This multi-layered testing approach is crucial for maintaining a robust defense.

Actionable Steps and Evidence

- Conduct Quarterly Vulnerability Scans: Run internal and external network vulnerability scans at least quarterly and after any significant change in the network. These scans must be performed by an Approved Scanning Vendor (ASV).

- Perform Annual Penetration Testing: Engage a qualified, independent security assessor to perform both network-layer and application-layer penetration testing at least once a year and after significant infrastructure or application upgrades.

- Implement Intrusion Detection/Prevention: Deploy intrusion detection systems (IDS) and/or intrusion prevention systems (IPS) to monitor traffic at the perimeter of the CDE and at critical points within it. Keep all signatures and rules up to date.

- Use Change-Detection Mechanisms: Implement file-integrity monitoring (FIM) tools to alert personnel to unauthorized modifications of critical system files, configuration files, or content files. FIM checks should be performed at least weekly.

- Document and Remediate: Maintain detailed records of all testing activities, including scan reports, penetration test findings, and remediation actions taken. Auditors will require proof that you not only found vulnerabilities but also fixed them according to their risk ranking. For a deeper understanding of this process, you can explore some software testing best practices which share similar principles.

12. Requirement 12: Maintain a Policy That Addresses Information Security for All Personnel

A strong information security policy is the cornerstone of your PCI DSS compliance checklist, providing the official framework that governs all security practices. This requirement mandates the establishment, publication, maintenance, and dissemination of a formal security policy that outlines acceptable use, defines roles and responsibilities, and sets clear security expectations for all personnel, including employees, contractors, and vendors. It ensures everyone understands their role in protecting the Cardholder Data Environment (CDE).

This policy acts as the authoritative source for security governance, ensuring consistent application of controls across the organization. For example, a financial institution would use this policy to enforce strict access controls for its core banking system developers and to mandate annual security awareness training for its customer service representatives, creating a unified security culture. A well-documented policy is a critical piece of evidence for auditors, demonstrating that security is a formalized and managed process.

Actionable Steps and Evidence

- Develop a Comprehensive Policy: Create a formal, written information security policy that covers all PCI DSS requirements. This document should serve as the master guide for your entire security program.

- Define Roles and Responsibilities: Clearly document security roles and responsibilities for all personnel. Your policy must explicitly state who is accountable for managing firewalls, reviewing logs, and responding to incidents.

- Establish Annual Security Awareness Training: Implement and document a mandatory security awareness program for all team members upon hiring and at least annually thereafter. Evidence includes training logs, materials, and attendee acknowledgments.

- Review and Update Annually: The policy is a living document. Conduct a formal review at least once a year or after any significant environmental changes to ensure it remains relevant and effective. Maintain a version history as evidence for auditors.

- Acknowledge and Distribute: Ensure all personnel read and formally acknowledge that they understand the policy. Maintain signed acknowledgment forms or digital records as proof of compliance.

PCI DSS 12-Point Compliance Comparison

| Requirement | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases | Key advantages |

|---|---|---|---|---|---|

| Install and Maintain a Firewall Configuration | Medium–High | Network engineers, firewall appliances/config, logging | Segmented network and controlled traffic flows to CDE | Perimeter/zone segmentation, DMZs, cloud VPCs | Reduces attack surface; improves traffic visibility; supports compliance |

| Do Not Use Vendor-Supplied Defaults | Low–Medium | Operational time, configuration management, deployment automation | Eliminates common default-credential entry points | Initial provisioning, base images, large infrastructure rollouts | Quick risk reduction; easy to automate; prevents automated attacks |

| Protect Stored Cardholder Data | High | Encryption tools, KMS/HSM, key management, developer effort | Data remains unreadable if storage is compromised | Databases, backups, archives containing PAN/SAD | Reduces breach impact; regulatory alignment; customer trust |

| Encrypt Cardholder Data in Transit Across Public Networks | Low–Medium | TLS certificates, cipher configuration, monitoring tools | Prevents interception and MITM on public networks | APIs, mobile apps, web transactions, remote admin access | Industry standard protection; broad platform support; low perf impact |

| Protect Systems Against Malware and Maintain Anti‑Malware Software | Low–Medium | Endpoint/EDR agents, centralized management, signature updates | Blocks known malware and provides detection/response | Desktops, servers, developer workstations, test environments | Centralized threat visibility; straightforward baseline protection |

| Develop and Maintain Secure Systems and Applications | High | SDLC processes, SAST/DAST tools, training, security engineers | Fewer vulnerabilities delivered to production; faster remediation | Application development, CI/CD pipelines, third‑party code | Prevents vulnerabilities early; improves code quality and accountability |

| Implement Strong Access Control Measures (Least Privilege) | Medium | IAM systems, RBAC design, PAM, MFA | Access limited to business-need users; improved auditability | Multi-team environments, privileged admin access, cloud infra | Minimizes insider risk; enforces accountability; limits blast radius |

| Identify and Authenticate Access to System Components | Medium | Identity management, MFA, tokens/certificates, logging | Reliable user/service identification and traceability | Remote/admin access, APIs, service accounts | Strong authentication; supports audits and incident response |

| Restrict Physical Access to Cardholder Data | Medium | Badges/biometrics, CCTV, visitor controls, secure disposal | Prevents theft/tampering of hardware and media | Data centers, server rooms, on-prem backup storage | Protects physical assets; prevents hardware-based attacks |

| Track and Monitor Access to Network Resources and Cardholder Data | High | SIEM/log aggregation, storage, analysts, alerting | Timely detection, forensics, and compliance evidence | CDE monitoring, incident response, audit preparation | Enables rapid detection and investigation; provides audit trails |

| Regularly Test Security Systems and Processes | Medium–High | Vulnerability scanners, penetration testers, test frameworks | Identifies control gaps and validates security effectiveness | Quarterly scans, annual pentests, CI/CD security checks | Proactive vulnerability discovery; validates controls before exploitation |

| Maintain a Policy That Addresses Information Security for All Personnel | Low–Medium | Policy authors, training programs, governance and enforcement | Consistent security expectations and documented responsibilities | Organization-wide security baseline, onboarding, vendor management | Establishes governance and culture; supports compliance and training |

From Checklist to Culture: Your Next Steps in PCI DSS Compliance

Navigating the 12 core requirements of the Payment Card Industry Data Security Standard is a formidable task, but this comprehensive PCI DSS compliance checklist has laid the groundwork for your success. We have moved beyond surface-level descriptions, diving into the actionable tasks, evidence collection, and common pitfalls associated with each control, from securing your network with robust firewall configurations (Requirement 1) to maintaining a vigilant information security policy (Requirement 12). The journey you've just taken through each requirement is designed to be more than a simple to-do list; it is a strategic blueprint for building a secure and resilient cardholder data environment (CDE).

The true takeaway is that PCI DSS compliance is not a one-time project to be completed and forgotten. Instead, it is a continuous, cyclical process of assessment, remediation, and monitoring. Achieving compliance is a milestone, but maintaining it is the ultimate goal. This shift in perspective, from viewing compliance as a burdensome audit to embracing it as a core business function, is what separates vulnerable organizations from secure ones. It's the difference between merely checking a box and fundamentally embedding security into your operational DNA.

Key Takeaways and Immediate Actions

To translate this knowledge into tangible results, your focus should now turn to a structured and prioritized action plan. The most effective strategies move beyond a reactive stance and build proactive security habits.

- Move Beyond the Checklist Mentality: The 12 requirements are not isolated silos. A failure in access control (Requirement 7) directly impacts your ability to monitor network resources (Requirement 10). Weak development practices (Requirement 6) can render your anti-malware solutions (Requirement 5) ineffective. Recognize these interdependencies and adopt a holistic security strategy where each control supports the others.

- Embrace 'Business as Usual' Compliance: Your goal is to make security an everyday activity. This means integrating security scans into your CI/CD pipeline, making log reviews a daily operational task, and conducting regular, small-scale access reviews instead of a massive annual audit. This approach makes compliance manageable, less disruptive, and far more effective at catching threats early.

- Prioritize Risk-Based Remediation: After completing your initial gap analysis using this checklist, you will likely have a list of vulnerabilities and non-compliant controls. Don't try to fix everything at once. Prioritize your efforts based on risk. A missing patch on a public-facing web server presents a far greater immediate threat than an outdated policy document stored on an internal-only server. Address the most critical gaps first to achieve the greatest reduction in risk with the resources you have.

The Strategic Value of Sustained Compliance

Mastering the principles within this PCI DSS compliance checklist delivers benefits that extend far beyond avoiding fines and penalties. A strong compliance posture is a powerful business enabler and a competitive differentiator. It builds trust with your customers, who are increasingly aware of data security risks. It enhances your brand reputation, demonstrating a commitment to protecting sensitive information. For our clients in fintech, e-commerce, and enterprise SaaS, this trust is the currency of modern business.

Furthermore, the operational discipline required for PCI DSS-from meticulous documentation to regular testing-often leads to more efficient, stable, and reliable IT systems. By enforcing best practices in network segmentation, access control, and secure coding, you are not just achieving compliance; you are building a higher-quality, more secure digital product. This proactive stance protects your revenue, safeguards your customers, and positions your organization as a trustworthy leader in your industry. The effort invested in moving from a simple checklist to a deeply ingrained security culture is an investment in your company's long-term viability and success.

Transforming this checklist into a living, breathing security program requires deep expertise in secure infrastructure, development, and DevOps. Group 107 specializes in engineering secure, compliant, and scalable digital platforms that embed these principles from day one. To ensure your compliance journey is built on a solid foundation, connect with our security and DevOps experts today.